BY FERNANDO DE FRUTOS, CFA, PhD | CIO BOREAL CAPITAL MANAGEMENT | 24 JUNE 2021

• After having managed to deny the inevitable without losing credibility, the Fed has surprised the market by shortening the timetable for the first rate hikes and tapering of asset purchases. The reason has been that the economy continues to recover faster than expected, which is a very positive development

• Although the economy still has a long way to go until 2023, and a rate hike more or less by then is no big deal, the market has interpreted the change in stance as a sign that the Fed will not let inflation get out of control

• The policy precedent set by the successful – but unusually generous – economic management of the pandemic poses the risk of validating its use in less exceptional circumstances. By beginning to decouple monetary policy from fiscal policy, the Fed has not only marked its independence, but also calmed financial markets, reducing pressure on long-term interest rates

Jay Powell’s press conferences leave the listener wondering whether one is being the victim of a sort of mind trick, or listening to a tongue twister. From “we are not even talking about talking about” (referring to tapering asset purchases), to labeling the latest FOMC as the “talking about talking about” meeting.

The Fed has a long tradition of resorting to obtuse language, dating back to its Jedi Grandmaster, Chairman Greenspan; who left a legacy of phrase-riddles to remember, such as: “I know you think you understand what you thought I said but I’m not sure you realize that what you heard is not what I meant”.

The new Fed chair, by contrast, has radically changed tactics; he speaks with crystal clarity, but elevating the discussion to the meta-meta level; a kind of quantum monetary world where, like Schrödinger’s cat, one thing and the opposite can happen at the same time; or happen not to happen; in Powell’s parlance.

This game of smoke and mirrors is for the sole purpose of keeping all options open. In the old days, when monetary policy enjoyed great room for maneuver, this calculated ambiguity allowed the Fed to surprise the market. But today, with interest rates at zero, the goal is to try not to unnecessarily unsettle financial markets.

In the past, the market was wary of the Fed, who was seen as the responsible adult in charge of “taking away the punch bowl”; ending the party before the economy could overheat. Nowadays, instead, the Fed is like a father trying to find ways not to upset a spoiled child, who always asks for more jelly beans and is notoriously famous for throwing tantrums.

In this respect, the recent policy shift does not represent a great change; something like threatening to take the goodies away if the school grades in a few years are not good enough. Bearing in mind that the average business cycle lasts less than 5 years, the kid has reacted with a “we’ll see” attitude.

However, the true recipient of the message has not been the market. The Fed also plays cat and mouse with other actors who influence (and are influenced by) its monetary policy: commercial banks transmitting it, other central banks whose decisions affect the dollar, and finally, the federal government, which sets the fiscal policy.

The relationship between the Fed Chairman and the US President is often a tug of war. In a recession, monetary and fiscal policy must work in tandem, but when the recovery begins, the central bank often becomes a constraint on the government. For example, Trump’s pro-cyclical fiscal stimulus provided the excuse for Janet Yellen to begin normalizing interest rates; while Robert Rubin and Alan Greenspan struck a bargain whereby the Fed maintained an accommodative policy, in exchange for the US Treasury reducing the fiscal deficit. This contributed to lengthening the economic cycle, and to run a fiscal surplus for the first (and last) time since 1969.

Exiting a crisis is tricky, and requires some coordination. After the financial crisis, for example, central banks had to continue to do all the heavy lifting, while governments retreated into austerity. That is why when the pandemic broke out, governments were urged to act with courage this time.

Initially, the Fed encouraged the government to do too much rather than too little. But as the saying goes, “be careful what you wish for”. The latest stimulus package passed by President Biden exceeded all expectations and, along with a more rapid reopening thanks to the success of the vaccination program, provided a major boost to the economy, stoking inflationary fears.

Fed members are, after all, human beings, with careers and reputations to protect; and continuing to deny the possibility of considering a policy normalization in these circumstances, was beginning to make them seem disconnected from reality, or worse still, accomplices of the government. Furthermore, if fiscal policy is finally taking the baton, it makes sense for monetary policy to start decoupling, in order to be ready to intervene when the next crisis hits.

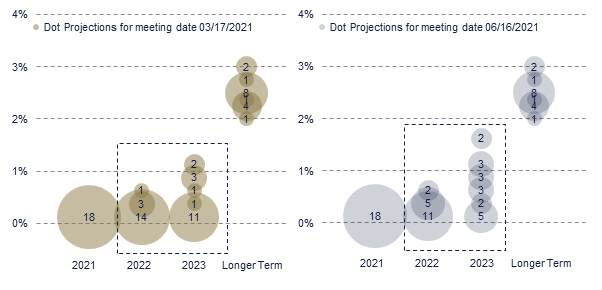

The change in the “Fed dots” is a first step in that direction, although more symbolic than anything else. Fed members know how difficult it was to begin to normalize monetary policy after the financial crisis; and the gap that separates its long-term projections (or, rather, “aspirations”) from current interest rates, seems impossible to bridge.

The Fed would welcome slightly higher inflation, if it were accompanied by robust economic growth. However, it needs to calibrate carefully in order not to risk its independence. The biggest threat is that the precedent set by the pandemic will tempt politicians to use the fiscal bazooka when faced with a “normal” recession. After all, the old adage “never waste a good crisis” has taken on a different meaning, with the government giving away money almost indiscriminately to citizens and businesses.

In short, Jay Powell has managed to pivot from a corner, thereby initiating the process of disconnecting monetary policy from fiscal policy. And by stating that he will not let inflation get out of control, he has also brought long-term interest rates down (once the market deciphered the message). Not bad for a Jedi apprentice!

* This document is for information purposes only and does not constitute, and may not be construed as, a recommendation, offer or solicitation to buy or sell any securities and/or assets mentioned herein. Nor may the information contained herein be considered as definitive, because it is subject to unforeseeable changes and amendments.

Past performance does not guarantee future performance, and none of the information is intended to suggest that any of the returns set forth herein will be obtained in the future.

The fact that BCM can provide information regarding the status, development, evaluation, etc. in relation to markets or specific assets cannot be construed as a commitment or guarantee of performance; and BCM does not assume any liability for the performance of these assets or markets.

Data on investment stocks, their yields and other characteristics are based on or derived from information from reliable sources, which are generally available to the general public, and do not represent a commitment, warranty or liability of BCM.