• Inferring that we may return to a 70’s-style inflation due to a repetition of the bad policy decisions of that time, is a rather simplistic reading of economic history. Despite the fact that both periods can be characterized by ultra-loose fiscal and monetary policies, inflation this time is a supply-side problem caused by restrictions related to the pandemic; and the stimulus was essential to avoid a protracted contraction.

• Considering that long-term interest rates have barely budged, despite inflation levels not seen in decades, valuation risk remains rather low for equities. The biggest risk is that if inflation does not abate, the Fed may be forced to raise interest rates to a point that causes the economy to slow down. Our central scenario however remains that supply chain bottlenecks will be resolved, and secular deflationary forces will prevail.

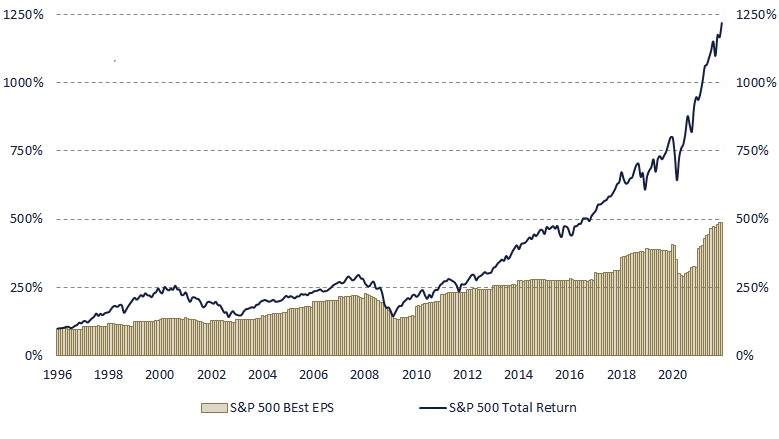

• Barring an economic slowdown, corporate earnings will determine stock market returns in 2022. While it is true that the (unexpected) boost to earnings experienced in the wake of the pandemic may prove to be unsustainable, it is also worth considering that many companies continue benefiting from an accelerating digital transformation. And with real interest rates deeply in the red, the opportunity cost of not staying invested is higher than ever.

After three consecutive years of extraordinary equity markets returns – the last two while the economy was being savaged by the pandemic – investors, as in the famous song of The Clash, are singing to themselves: “Should I stay or should I go?”

Many see similarities between the historical period that preceded said song, and our time. When punk-rock emerged in the mid-1970s, the world economy was mired down by persistent inflation; caused in large part by growing union power coupled with misguided monetary and fiscal policies. The concern is that the comparisons do not end there, and that as happened back then we will suffer another lost decade for equity markets.

But comparative history requires us to be very careful with the context. Lessons were learned from that period, and in 1982, when the band released their most celebrated song, the economic policies that had led to high inflation were beginning to reverse in full force; ushering in the period of greatest macroeconomic stability ever experienced.

In the decades that followed the charge against inflation led by Chairman Volcker, corporate profits boomed. The liberalization of trade and finance (accelerated after the fall of communism), as well as the productivity increases brought about by the introduction of personal computers and the Internet, also contributed greatly.

We are still benefiting vastly from these events, which have not only contributed to global economic growth, but have also proven to be key to keeping inflation in check. Offshoring (or the threat of it) significantly reduced collective bargaining power in developed countries; and technology, combined with globalization, contributed to the drastic cheapening of many goods and services.

To infer that because we have had a bout of inflation we are going to go straight back to the 70s is a very naïve interpretation of economic history. The pandemic has altered the prevailing economic regime in the short term, but it hardly has the potential to fundamentally change it. It is supply-side constraints that have been responsible for the recent surge in inflation, not fiscal and monetary largesse. In fact, without the support from governments and central banks we would have experienced a deep (and deflationary), recession.

Proof that past mistakes are unlikely to be repeated is that the Fed has announced (earlier than expected) that it will begin to dial down its support. Therefore, the main risk for the economy is not falling into a 70s-style stagflation trap, but rather that the dose of stimulus has had to be so disproportionate that reducing it can easily cause “withdrawal symptoms”.

This helps explain the apparent paradox of long-term interest rates remaining stubbornly low while inflation reaches levels not seen in decades, all while the Fed is about to begin tightening. The reading is clear, the bond market is discounting that either inflation eases, or the Fed will have no choice but to cool demand to prevent a price spiral.

For investors, the key takeaway of all that has happened in 2020 is that the thesis of “lower for longer” interest rates has successfully passed an extreme stress test. If rates have barely increased, despite inflation nearing 7%, when will they?

With this in mind, investors should not be overly concerned about a valuation shock. However, they do have to worry about the sustainability of the recovery, as any sign that the economy is slowing down could cause a major correction in equity markets. With this in mind and contrary to the prevailing narrative, Growth stocks should be less vulnerable than Value and Cyclicals.

In a way, the year that begins marks the return of “business as usual” for investors; with corporate profits back to center stage. And here the risk goes both ways. On the one hand, we can see a reversal to the historical trend, given that the pandemic appears to have provided a counterintuitive boost to earnings. But on the other hand, the trend may continue as long as the corporate world continues to profit (with winners and losers) from the digitization push; something that the pandemic has accelerated even further.

This is the implicit wager of being long equities. The only certainty we have is that it will be next to impossible to repeat a year like 2021, in which all S&P 500 sectors had positive returns, and the index reached 70 new highs. But since bonds hardly offer an alternative, the opportunity cost of not staying invested is simply too high if a correction does not finally occur. Or giving a twist to the song, “If I stay there will be trouble (…) And if I go it will be double (…)”

Fernando De Frutos. Chief Investment Officer.

* This document is for information purposes only and does not constitute, and may not be construed as, a recommendation, offer or solicitation to buy or sell any securities and/or assets mentioned herein. Nor may the information contained herein be considered as definitive, because it is subject to unforeseeable changes and amendments.

Past performance does not guarantee future performance, and none of the information is intended to suggest that any of the returns set forth herein will be obtained in the future.

The fact that BCM can provide information regarding the status, development, evaluation, etc. in relation to markets or specific assets cannot be construed as a commitment or guarantee of performance; and BCM does not assume any liability for the performance of these assets or markets.

Data on investment stocks, their yields and other characteristics are based on or derived from information from reliable sources, which are generally available to the general public, and do not represent a commitment, warranty or liability of BCM.