- We are in the midst of a crisis that cannot be easily compared to any other experienced before. This generates great uncertainty, which is reflected in unprecedented market volatility. However, from an investment perspective, this is “business as usual”, given that in every major crisis we find ourselves facing uncharted territory.

- Each crisis has unique causes, just as fiscal and monetary responses are also idiosyncratic. In the current crisis, the latter have been overwhelming, and should be largely enough to avoid a permanent economic loss. However, financing these efforts will be costly, and neither the finances of the countries nor the balance sheets of the companies are all in the same good shape. Therefore, there will be some casualties among them.

- One of the few common denominators in any crisis is that the winners always emerge from them strengthened. We believe that we continue to witness an unprecedented pace of innovation, which will not be affected by the current crisis; and leading companies will soon recover their rate of revenue generation. Therefore, the best recipe for uncertainty is to stay invested in quality assets, knowing that regardless of the form the recovery takes, we can avoid a permanent loss of capital.

When we are faced with a new problem, for which there is no methodologically proven way of solving it, we often resort to so-called “heuristic” solutions. The term refers to strategies that, although imperfect, help us find an approximate solution to the problem in question; This is very useful when the information we have is insufficient, or when achieving a greater degree of precision does not compensate for the time spent on it. One of them is the so-called “familiarity heuristic”, which consists of resorting to similar episodes to contextualize a new and complex situation; such as the one we are currently experiencing.

As the crisis began to unfold, analysts quickly turned to comparable events to determine the potential economic and health costs of the epidemic. The SARS (2002) and MERS (2012) outbreaks, caused by other coronavirus strains, were the first obvious comparisons. The fact that both resulted in “near misses”, as the global spread of the disease could finally be contained, provided a false sense of security for both investors and health authorities.

When the new virus threatened to reach the pandemic stage, similarities were established with seasonal influenza and the H1N1 swine flu (2009). However, since the new virus has an unusually high reproduction rate and causes a greater number of severe cases than those, some people see the 1918 Spanish flu as the most appropriate comparison. However, this parallelism has very little informational power, since both economics and medical science are radically different today; we are not in the midst of a world war, and we have antibiotics and intensive care units.

In fact, the exceptional and dramatic nature of the current situation is such that it lends itself to being compared to times of war. But, while it is true that we see some productive resources being diverted to combat the pandemic, such as automobile manufacturers that produce ventilators, there has not been a change in supply and demand like the one that usually occurs during a war. There is also no loss of productive capital or human capital and, furthermore, we know that we will finally win this battle.

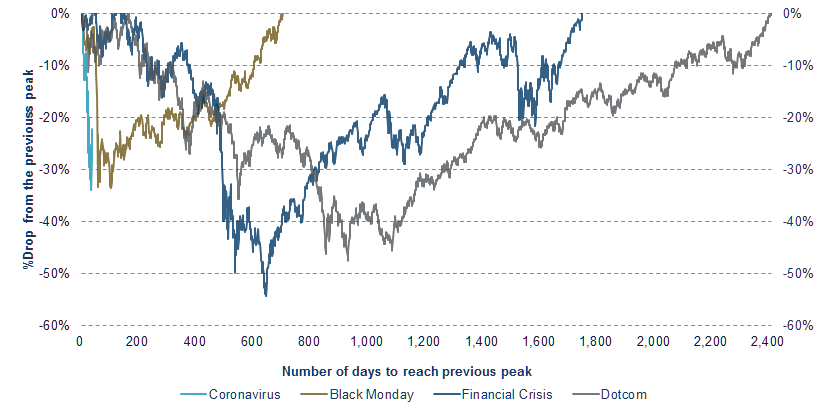

Historical comparisons aside, investors are busy these days trying to categorize the recent stock market crash, comparing it to other episodes in the past of a similar magnitude. Likewise, economists are trying to assess whether the recovery will follow a “V”, “U”, “W” or “L” shape. The problem with this type of “chartist” approach is that the complexity of the system does not lend itself to easy generalizations.

The fact is that each economic crisis is caused by a unique constellation of factors, and therefore market response is always idiosyncratic. Sometimes it is the market that causes the recession (Dotcom), sometimes the market and the economy fall in tandem (Financial Crisis), sometimes the market crashes for no apparent reason, and the economy continues as if nothing happened (Black Monday) and other times, as has happened in the current crisis, the market anticipates an incoming recession.

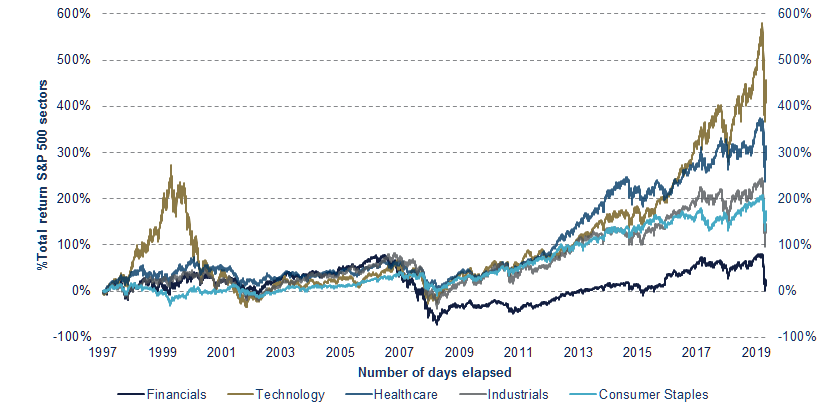

The interplay between the economy and the stock market depends on the underlying causes of the crisis, as well as the government’s response to it; so one can expect very disparate performances between geographical areas and sectors. The financial crisis is a good example: while the US quickly implemented measures to restore the financial system, allowing the economy to recover in a “V” shape, Europe was much more reactive, the ECB made a mistake by raising rates too soon, and the economy relapsed with the sovereign debt crisis, following a “W” shaped path. Likewise, after the crisis, the profitability of some sectors, notably banking, worsened dramatically; while that of other industries skyrocketed, buoyed by share buybacks, funded by extremely low interest rates.

The fiscal and monetary response to the current crisis in the main economies has been very decisive. Therefore, if, as we expect, the current pandemic subsides in the coming weeks, we should experience a recovery between a lowercase “v” and a capital “V”. The degree of growth will critically depend on the effectiveness of the measures implemented, as well as the long-term costs that these will entail.

Given that the current crisis has been caused by an external shock, and not by the reckless behavior of some economic agents, there is no “moral hazard” that prevents politicians from opening the state coffers. However, some are finding it difficult to resist viewing this opportunity as a “happy hour” to further their political agenda. But rest assured that the “bond vigilantes will return with a vengeance against those who profligate.

Unless there is an agreement to guarantee the debt of the weakest countries, which are also the most affected, Europe will probably lose a few more years compared to the United States and Asia. Emerging markets will also see their economic growth hindered as, although they are generally less indebted, they will have to postpone investments in infrastructure and education to cope with the economic impact of the virus.

At the sectoral level, the profitability of some industries will be radically affected. This crisis will accelerate the transition to online, which will impact retail, education, healthcare and the real estate sector amongst others. Travel and tourism will also have to adapt to new and expensive regulations; and, in more generally, there will be a rethink of the need to onshore production and promote national champions in strategic industries, such as pharmaceuticals.

But just as in previous crises, innovation and technological progress will hardly be affected. If anything, it will accelerate as we try to find solutions to a new problem. This will continue to increase inequality between countries, sectors, companies and individuals. And here, the “familiarity heuristic” helps us, since there is a clear common denominator in all crises: the winners emerge from them strengthened.

Our recommendation, from the investment point of view, is to avoid those assets whose profitability depends on getting right the bottom of the market, or the shape that the recovery takes. Large profits may be made by investing in stocks and bonds from airlines, hotels and energy companies, but the outcome is highly uncertain. On the contrary, we have one of the few certainties that this business has, knowing that quality companies will follow a recovery in the form of a square root “√”.

Fernando de Frutos – Chief Investment Officer

* This document is for information purposes only and does not constitute, and may not be construed as, a recommendation, offer or solicitation to buy or sell any securities and/or assets mentioned herein. Nor may the information contained herein be considered as definitive, because it is subject to unforeseeable changes and amendments.

Past performance does not guarantee future performance, and none of the information is intended to suggest that any of the returns set forth herein will be obtained in the future.

The fact that BCM can provide information regarding the status, development, evaluation, etc. in relation to markets or specific assets cannot be construed as a commitment or guarantee of performance; and BCM does not assume any liability for the performance of these assets or markets.

Data on investment stocks, their yields and other characteristics are based on or derived from information from reliable sources, which are generally available to the general public, and do not represent a commitment, warranty or liability of BCM.