BY FERNANDO DE FRUTOS, CFA, PhD | 6 APRIL 2023

- For more than a decade, central banks have been unable to raise rates, due to chronic subpar economic growth and high unemployment. With rates near the zero-bound, a mistake from overtightening could have been very costly to reverse. While central banks always had the tools at their disposal to deal with inflation.

- At the start of the pandemic, it looked as if interest rates were going to remain anchored at zero forever. But the unexpected burst of inflation turned monetary policy upside down. Betting on which monetary regime will prevail is very risky. In addition, recent problems in the banking sector could imply that a potential return to the low-rate environment may be the consequence of a deeper slowdown than initially thought.

- Increased uncertainty warrants more defensive positioning in portfolios, as investors need to assess a broader range of potential scenarios. Interest rates may fall more than previously discounted by the market; but the same can happen with corporate profits. All the above leads us to underweight risk assets and favor companies that enjoy secular growth and, therefore, can also benefit more from a potential drop in interest rates.

In the decade plus from the Great Financial Crisis to the pandemic, central banks proceeded with extreme caution, always trying to assuage markets and avoid adding stress to the system. In 2008, the collapse of the financial system had been so narrowly avoided that stability was sought above all else.

Policymakers knew that they had thrown the rulebook out of the window, but also that returning to orthodoxy, even if necessary, would be a long and risky journey. The Fed kept interest rates at zero for seven consecutive years and, as if this were not enough, launched successive rounds of Quantitative Easing. Other central banks followed suit, and even ventured to experiment with negative interest rates.

As the economy gradually recovered, monetary policy “normalization” was on every central bank’s wish list. This turned out to be an elusive target. The financial system had become addicted to easy money, presenting severe withdrawal symptoms every time the Fed threatened to “taper”. Fearful of disappointing markets, central banks resorted to what is known in the jargon as “forward guidance”; which in practice is nothing more than kicking the can down the road.

The threat of deflation was the “Boogeyman” that provided a convenient cover to hide an inconvenient truth. The economy had been growing beyond its means fueled by debt, and policymakers knew deleveraging was a lengthy process fraught with risks. Inflation, by contrast, had only turned negative for a brief interlude at the depths of the GFC. But for most of the next decade it remained close to, although slightly below, its official 2% target.

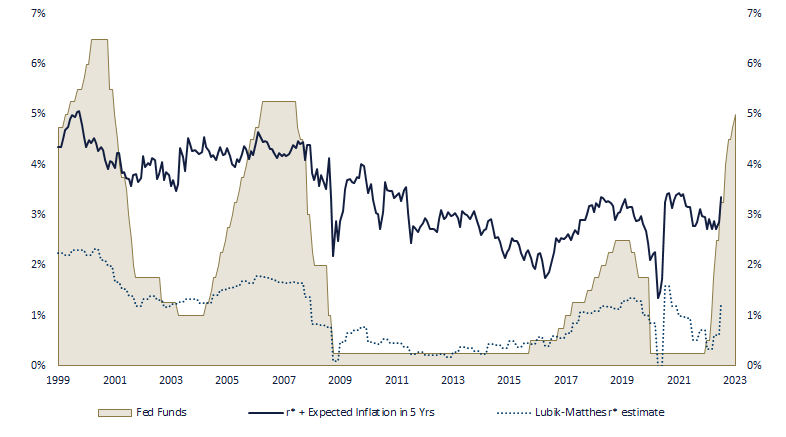

The natural interest rate r* (the theoretical, unobservable rate that would be neutral for the economy) had been declining for decades pushed down by structural factors and ended up collapsing after the financial crisis. In such an environment, raising interest rates presented an asymmetric risk, as central banks had little room to correct a potential mistake.

Several “near crisis” events punctuated this long cycle of monetary policy largesse, forcing the Fed to postpone the “liftoff” until late 2016, only to be forced to abort it two years later. Then the pandemic hit, and interest rates plunged to new lows. That same summer, the Fed published its new rulebook, which would tolerate higher inflation to compensate for previous periods of slow nominal growth.

At this point we reached the equivalent of “Zero Kelvin” in interest rates, with Chairman Powell saying that “they were not even thinking about thinking about raising them” (the ultimate form of forward guidance). What happened next is well known. Overgenerous fiscal policies, combined with supply-side restrictions, led to a sudden burst of inflation. Later exacerbated by the impact of the war in Ukraine on energy markets.

The Fed, still conditioned by the mindset of the previous decade, was initially cautious and promised patience and a measured approach. Then, as inflation reached levels not seen in decades, went into panic mode. Suddenly, the narrative changed, and inflation became the new “monster” that made it necessary to raise rates in a sprint.

Such a sudden and steep change in interest rates, from such a low starting level, was unprecedented. Something had to break, especially considering how years of ultra-accommodative monetary policy have contributed to the froth in the housing market, as well as ballooning corporate and government debts. What nobody expected was that the first cracks would appear (once again) in the financial sector.

With a credit crunch on the horizon, the job of central banks has become much more difficult. Now they will have to juggle three objectives: inflation, economic growth, and financial stability. It has also made life more difficult for investors, who must reassess how much further corporate profits may fall as a result of a deeper recession.

The other big unknown for investors is how fast and how deep interest rates will fall. One of the hottest academic debates right now concerns the fate of r*. It may well be that interest rates had been kept unnecessarily low for too long, and that the inflation shock has helped expose this policy mistake. But it could also be that central banks have overtightened, and the economy will start to sputter if they do not reverse course.

Given that trying to forecast the path the economy will take is more difficult than usual, an underweight in risk assets seems like the most sensible course of action. In addition, investors should favor those companies that enjoy secular growth (therefore better equipped to weather a downturn) and that will eventually benefit most from falling interest rates.

Like Alice in “Through the Looking-Glass”, central banks seem to have entered a reverse reality. Where the problem is inflation, while the economy is always growing, and jobs are plentiful. But they may wake up from their dream to see themselves as the main character in another famous story: “The Emperor’s New Clothes”.

Their newfound zeal as inflation watchdogs has been met with widespread market disbelief, manifested in the record inversion of the yield curve. And like the child who shouts in the parade that the emperor is naked, the sudden implosion of two regional banks has served to expose the true state of affairs.

Unfortunately, mimicking the emperor in parade, the Fed and the ECB have continued to pretend, raising interest rates as if nothing had happened.

* This document is for information purposes only and does not constitute, and may not be construed as, a recommendation, offer or solicitation to buy or sell any securities and/or assets mentioned herein. Nor may the information contained herein be considered as definitive, because it is subject to unforeseeable changes and amendments.

Past performance does not guarantee future performance, and none of the information is intended to suggest that any of the returns set forth herein will be obtained in the future.

The fact that BCM can provide information regarding the status, development, evaluation, etc. in relation to markets or specific assets cannot be construed as a commitment or guarantee of performance; and BCM does not assume any liability for the performance of these assets or markets.

Data on investment stocks, their yields and other characteristics are based on or derived from information from reliable sources, which are generally available to the general public, and do not represent a commitment, warranty or liability of BCM.