- Equity markets appear to have long been disconnected from the dire economic reality caused by the pandemic; with stocks near all-time highs, while the economy is still running significantly below its potential capacity.

- One of the reasons for this divergence has been the unprecedented fiscal and monetary support, which has made it possible to avoid the typical negative feedback loop that usually occurs in recessions – when consumption and investment are scaled down, accentuating the slowdown. This has allowed investors to look beyond the crisis, and thereby stabilize financial markets.

- But the main driver behind the strong rally in equity markets has been the dramatic shift in interest rates. Until recently, the US dollar had managed to avoid the „zero interest rate trap“ that other currencies had fallen into, but now it seems almost inevitable that it will follow the same path. Due to the dominant role that the dollar plays in the financial system, this has huge implications for the valuations of all asset classes. And among them, equities continue to look the most attractive.

Something seems out of place, with equity markets approaching their all-time highs, as we are in the midst of an unprecedented economic recession. A crisis of global reach that, after the sudden stop caused by the lockdowns, has left the economies operating at 80-90% of their capacity; and with some sectors, such as travel and hospitality, facing an existential threat.

Two explanations can be found for this apparent new bout of „irrational exuberance“. The first is the „comprehensibility“ of this crisis. Unlike other recessions, whose causes were attributed to concepts that were arcane for the average citizen (such as subprime mortgages), in this crisis anyone can grasp why we are in a deep hole.

In fact, this time it is as simple as it gets. We have been knocked down by a virus. A shock that can be considered a hybrid between a war and a natural disaster. A distinguishable enemy, sent by Mother Nature, but without causing the damage to infrastructure and the misallocation of productive resources that occur in an armed conflict.

The simplicity and indiscriminate nature of this crisis has also greatly played in favor of the swift and proportionate government response; this time unhindered by “moral hazard” considerations. The clear script of this crisis, consisting of keeping the economies on artificial life support until a vaccine arrives, has helped economic agents to keep their cool; thus avoiding the typical cuts in consumption and investment that feed back recessions.

All of the above, however, could speak for a stabilization in financial markets, but not the unprecedented rebound we have witnessed. After all, except for a few stocks that have benefited from the pandemic, most companies are facing several quarters of declining profits, until the economy returns to its pre-crisis level; something that can happen at the end of 2021 in the most optimistic scenario. How then can we be testing all-time highs on the S&P 500?

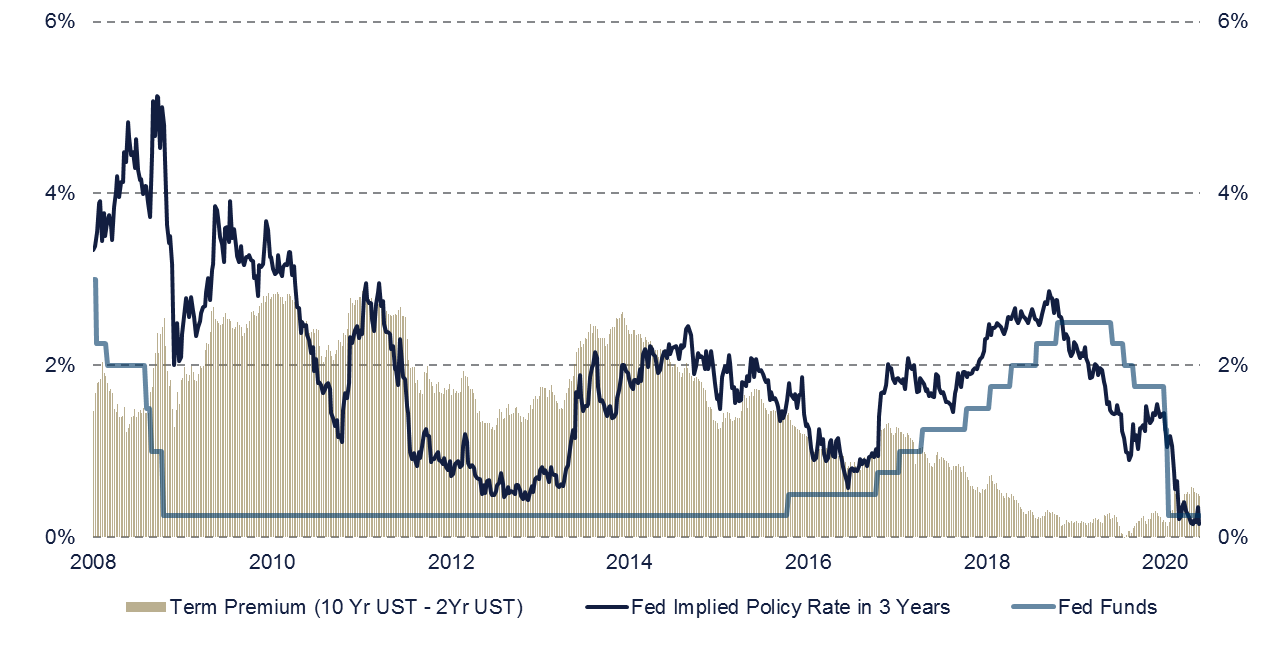

To find a rational explanation for this seemingly irrational behavior, one needs to look at the radical measures adopted by the Fed, as well as the dramatic shift in interest rate expectations that they have led to. We are witnessing the endgame of a multi-decade trend of falling interest rates.

The decline began in the 80s when central banks gained their independence, it was later fueled by deflationary forces such as globalization, technology and lower trend-growth as a result of an aging population. Finally, the Great Financial Crisis forced central banks to lower rates to zero, and even to resort to unorthodox measures, such as QE and negative rates.

The playbook that the Fed has followed during the current crisis largely resembles that of 2008. However, the measures adopted at that time were widely regarded as temporary in nature. And although the Fed had to postpone the normalization of its monetary policy for a period of seven years, markets never stopped considering the situation as a mere anomaly. As a result, long-term interest rates remained relatively high, with zero short-term rates not being fully distilled into equity valuations.

The big difference now is that, unlike in the past decade, both financial markets and the Fed (not to mention highly indebted governments) expect interest rates to remain extremely low in the coming years (See graph below). This is a completely new environment for investors because, although long-term rates had already turned negative in other currencies, the dollar, the anchor of the financial system, still allowed investors to obtain positive risk-free returns.

In this new reality, quality stocks, which still offer a 4% premium over Treasury yields, stand out as the most attractive asset class. Investors are gradually realizing that very few sources of yield remain available, and they are flocking into these stocks; just as people stockpiled toilet paper in anticipation of the lockdowns.

However, this form of hoarding is much more rational, since, unlike toilet paper, where it was not expected that there would be a shortage, investors are going to be deprived of returns for many years to come. And although with stocks on the verge of reaching new highs, succumbing to this mania may seem like a dummy thing, there is no alternative but to catch the few positive yields available; before they become an endangered species.

Fernando de Frutos – Chief Investment Officer

* This document is for information purposes only and does not constitute, and may not be construed as, a recommendation, offer or solicitation to buy or sell any securities and/or assets mentioned herein. Nor may the information contained herein be considered as definitive, because it is subject to unforeseeable changes and amendments.

Past performance does not guarantee future performance, and none of the information is intended to suggest that any of the returns set forth herein will be obtained in the future.

The fact that BCM can provide information regarding the status, development, evaluation, etc. in relation to markets or specific assets cannot be construed as a commitment or guarantee of performance; and BCM does not assume any liability for the performance of these assets or markets.

Data on investment stocks, their yields and other characteristics are based on or derived from information from reliable sources, which are generally available to the general public, and do not represent a commitment, warranty or liability of BCM.