Nobel Prize-winning economist R.J. Schiller is the father of “Narrative Economics”. This new branch of research tries to understand how certain narratives about the state of the economy can spread virally and end up feeding back the main macroeconomic variables.

Currently, investors are particularly baffled by the unstoppable march towards negative interest rates worldwide, a trend that has been revived once the Fed has capitulated abruptly, abandoning any hope of normalizing interest rates.

There are two main narratives that try to make sense of the «Alice in Wonderland» environment in which we live, where banks are paying customers for taking mortgages and profligate governments can issue bonds at ridiculously low interest rates.

Under the “secular stagnation” narrative, low interest rates arise from subpar nominal growth, as a result of weak aggregate demand and strong deflationary forces. The antagonist narrative, however, explains low interest rates as a sign that the market is bracing for an incoming recession and the complete “Japanization” of the global economy.

Evidence for a recession is mixed so far, since we can observe a global slowdown in manufacturing as a consequence of the uncertainties surrounding the Trade War, but a resilient service sector, record-low unemployment, and strong consumer confidence.

But, even if the odds of the two narratives were equal, their asymmetric impact on portfolios has profound implications for risk management. Both scenarios speak in favor of long-term assets, since interest rates are likely to remain depressed, but a hardly existent term-premium in bonds, limits the gains that can be obtained at this point if the economy plunges into a recession.

A very healthy equity risk premium on the contrary, provides some cushion against a deceleration of earnings, or an increase in interest rates, while it allows to participate from a price appreciation via multiple expansion.

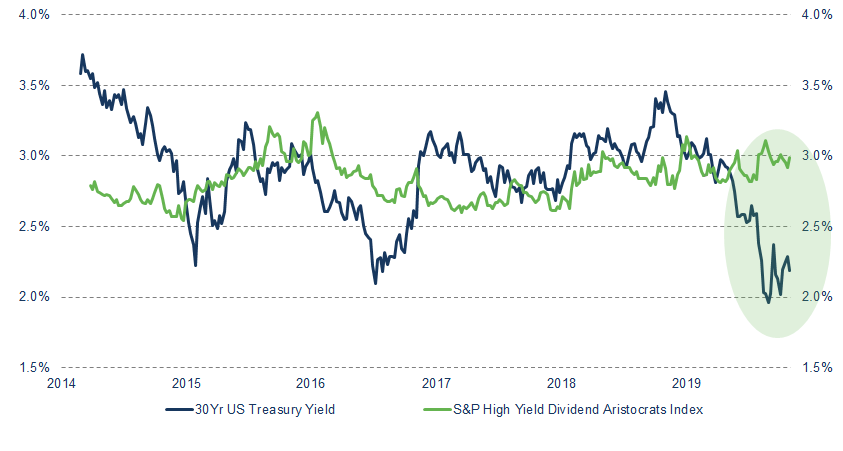

To help put into context, if you were to invest your pension money, what would you prefer to buy: a 30-Year US Treasury bond offering you 2.2% and make you pray that inflation does not return to its average during the period? Or the S&P High Yield Dividend Aristocrat Index that yields close to 3% and offers, with great probability, a potential capital appreciation in the long term?

If, however, you decide to opt for the deflationary narrative, and seize the «opportunity» to buy the 100-year Austrian bond that still yields a positive 1%, keep in mind that you have a much smaller margin of error; and that a small miscalculation can lengthen your working life or, worse, shorten your life expectancy.

Fernando de Frutos – Chief Investment Officer

* Este documento es puramente informativo y no constituye recomendación de compra de los activos financieros mencionados en el mismo. Ninguna información contenida en este artículo puede ser considerada definitva, dado que el objeto sobre el que se informa está sujeto a cambios y modificaciones).

Rendimientos pasados no garantizan rendimientos futuros, y en ningún caso la información vertida en esta página web pretende sugerir que rendimientos establecidos en este documento se obtendrá en el futuro.

La información ofrecida por BCM sobre el estado, desarrollo o evaluación de los mercados o activos específicos no debe interpretarse como un compromiso o garantía de rendimiento. Al respecto, BCM no asume ningunaresponsabilidad por el rendimiento de estos activos o mercados.

Los datos sobre inversión, rendimientos y otros aspectos se basan en o derivan de la información de fuentesconfiables, generalmente a disposición del público, y no representan un compromiso, garantía o responsabilidad deBCM.