- As the Covid crisis weighs heavily on a fatigued population, financial markets move closer to euphoria; clinging to a widely accepted narrative that economies will rebound strongly when herd immunity is achieved, while interest rates will remain extremely low

- Not all asset classes can justify their seemingly lofty valuations. Given that prices discount that the economy will recover strongly and steadily in the second half of the year, there is no room for disappointment. This risk is higher in credit markets where, unlike equities, the upside potential is much more limited.

- The long decline in interest rates have fueled assets returns over the past decades. But since everything indicates that we have reached the bottom, investors should brace for lower returns going forward. The positive news is that we are immersed in a wave of innovation that is rapidly transforming the economy, offering great opportunities to long-term investors.

After almost a year wrestling with the pandemic, fatigue begins to accumulate in the population. Yet surprisingly, as a third wave threatens with another harsh lockdown, the mood in financial markets is closer to euphoria than gloom.

This is a difficult thing to rationalize. It is true that catastrophic scenarios have been avoided, but the ability of the virus to continue spreading – despite greater protection measures and public awareness – continues to pose an existential threat to many sectors.

We know that these setbacks have been largely offset by the extraordinary news from the vaccine front; and that with monetary and fiscal support guaranteed, stock markets can afford to ignore the current situation.

But with some corners of the equity market exhibiting bubble-like behavior, one wonders if there is not excessive optimism. Investors are human beings, and it may be also the case that they are viewing stock markets as an escape from their daily miseries. A kind of avatar world, an aspiration that everything will return to normal one day. A psychological behavior similar to those who buy books because, unconsciously, they long for time to read them.

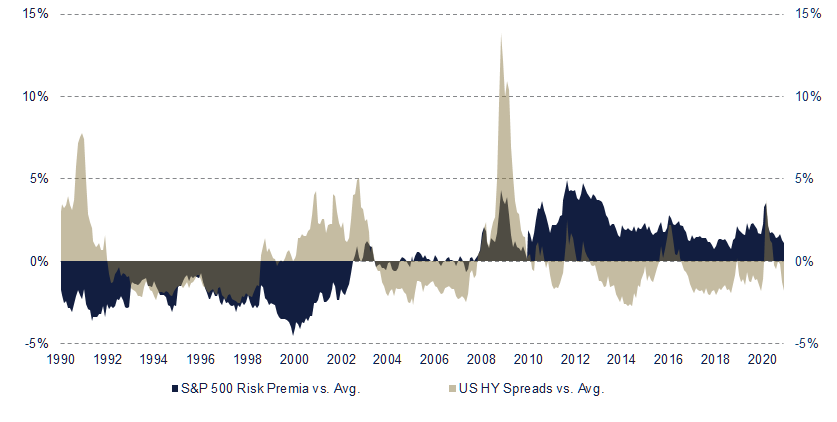

Changes in investor sentiment play a role in short-term market behavior, but for determining long-term returns, cold, hard data is a much better guide. In April, the equity risk premium was north of 5%, and buying stocks seemed like a no-brainer. However, currently, it has a less clear reading. Comparing with its historical average, valuations are still attractive; but there is an unprecedented dependency on interest rates that should dampen excessive optimism.

Credit markets, however, present a very different picture. High Yield and Emerging Markets spreads at the lower end of their spectrum. These are levels that are expected to be found when the economy is in very good health and markets are completely calm. This implies that any bump in the road can cause spreads to widen, thereby causing prices to fall. If to this is added that the risk-free rate is completely depressed, the margin to mitigate price fluctuations is currently very small.

Broad market performance will largely depend on how fast and how strong the economy returns to normal. The first is strongly dependent on the rollout of the vaccines, while the latter will depend on how consumers respond. Undoubtedly, there is a large pent-up demand that has not been fulfilled through digital channels, which will probably make the economy roar back. However, the medium-term steady state is harder to predict.

In aggregate terms, households have saved during the pandemic; and asset prices, from real estate to financial assets, have maintained or even increased in value. Thanks to this, consumer confidence has remained unusually high during a (monster) recession. However, it remains to be seen whether, when restrictions are lifted, households will spend happily, or rather decide to keep saving for what may come next.

Analysts expect corporate profits to rebound to a level close to pre-crisis level. Given that some sectors will continue to lag behind for a while, the rest of the economy will need to fire in all cylinders if investors are not to be disappointed.

At the same time, this growth outburst must occur without significantly altering long-term inflation expectations (there will surely be some price increases in the short term), as valuations are underpinned by interest rates remaining low for an extended period of time.

As asset prices are key for financial stability, the Fed has reassured markets that it will be patient, allowing inflation to overshoot before raising rates. But in the long run interest rates are determined by supply and demand, and if they fail to convince investors, there is a risk of a disorderly rise.

To the uncertainties about the timing and strength of the rebound, it must be added that we do not know to what extent the economy will have changed permanently. A good guess is that the great strides made in digitizing the economy during the pandemic will continue to drive innovation for years to come, and that many sectors will be transformed forever.

This will be a positive development in terms of productivity growth – contributing also to keep inflation under control – but will also entail costs. Painful adjustments will be necessary, and inequality at individual, corporate and country level will rise further. This can ultimately translate into redistribution policies between individuals, and tax harmonization between countries.

However, from an investment perspective, the timeframes of opportunities and risks are very different. Winners will reap the rewards immediately, while social adaptations to a post-pandemic world will take a long time to crystallize; in large part because inequality will continue to rise in a context of general rising welfare, and the debt burden will be spread over generations.

To sum it all up, there are many reasons to be optimistic about the medium and long-term prospects for stock markets. But the uncertainty in the short term is unusually high and should prevent us from falling into tactical distractions. Low interest rates, tight credit spreads, and a reasonable (but far from a bargain) risk premium, mean investors should prepare for lower returns in their portfolios going forward or, alternatively, adjust their risk appetite.

The latter does not necessarily mean falling into speculation, since another alternative is to extend the investment horizon beyond the customary year or two. This is not the time to (reluctantly) invest in stocks as a substitute for bonds. But if investors are willing to invest for the long term, the opportunities that are presenting themselves as the world accelerates into the third industrial revolution are unprecedented.

Fernando de Frutos – Chief Investment Officer

* This document is for information purposes only and does not constitute, and may not be construed as, a recommendation, offer or solicitation to buy or sell any securities and/or assets mentioned herein. Nor may the information contained herein be considered as definitive, because it is subject to unforeseeable changes and amendments.

Past performance does not guarantee future performance, and none of the information is intended to suggest that any of the returns set forth herein will be obtained in the future.

The fact that BCM can provide information regarding the status, development, evaluation, etc. in relation to markets or specific assets cannot be construed as a commitment or guarantee of performance; and BCM does not assume any liability for the performance of these assets or markets.

Data on investment stocks, their yields and other characteristics are based on or derived from information from reliable sources, which are generally available to the general public, and do not represent a commitment, warranty or liability of BCM.