FERNANDO DE FRUTOS, CFA, PhD | 24 MAY 2022

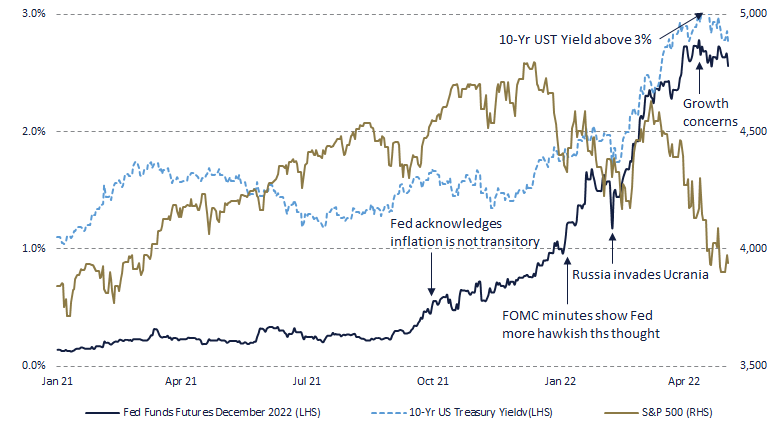

- After a decade characterized by low interest rates and subdued Inflation, both the Fed and a good part of the investment community have been resisting for almost a year to accept the new post-pandemic reality. In recent weeks however, it seems that we have witnessed a sort of capitulation, with the 10-year US Treasury bond yield clearly crossing the 3% threshold; further sinking stock and bonds prices.

- Paradigm shifts do happen, and the pandemic-driven changes in labor markets and supply chains may well prove more durable than initially thought. However, prudence advises us not to swap our investment thesis too soon. After all, the only solid empirical evidence is that current inflation is the result of a combination of factors that are, in principle, circumstantial: on the one hand, fiscal and monetary support measures aimed at preventing demand to collapse, and on the other the restrictions on the supply side caused by the pandemic.

- With stimuli being progressively withdrawn, anxiety is growing about the possibility of the economy falling into a recession. This is a plausible scenario if inflation doesn’t start to show signs of slowing down, and the Fed has no choice but to keep raising interest rates. Investors therefore must weigh carefully between the painful reality of a level of inflation not seen in decades, and the potential risk of a recession.

- Markets have corrected sharply in what looks like a perfect storm of narratives feeding back each other: sometimes falling on the impact of rising interest rates on asset valuations, and other times fearing its knock-on effect on growth. As a result, there is way too much pessimism priced in, since other more benign intermediate scenarios have been progressively abandoned. Therefore, long-term investors should stay invested, accepting the new valuations as a new starting point and not realizing losses out of panic.

Arguably, modern societies have become increasingly impatient, something stand-up comedian Ronny Chieng has masterfully captured in one of his Netflix specials. On the show he joked about American consumer’s dire need for a „Prime Now!“ service; since the 2-hour delivery currently offered by Amazon Prime is not fast enough (un-American!). Coincidentally, the show was recorded shortly before the pandemic hit and consumers had to seclude themselves in their homes. Back then, online shopping became both a lifeline and a pastime, which is at the root of the current bout of inflation.

US consumers, having received generous checks from the government that they could not spend on travel or restaurants, stormed the Internet in search of furniture, electronics and the like. And when thanks to the success of vaccines, economies began to reopen, they went after big game, such as cars or houses. Emerging from lockdowns with patience depleted and pockets replete they became price insensitive, since what mattered was enjoying the acquired good as soon as possible.

The surge in demand for goods coincided with restrictions affecting factories and ports due to the pandemic, which caused prices to rise. The tightness on the supply side was aggravated by an unprecedented recovery in the labor market; a vindication of government policies, which prevented a temporary halt of the economy from resulting in bankruptcies, job losses and another protracted recession like the one that followed the financial crisis.

The outbreak of inflation was initially considered as a secondary effect (of a temporary nature) caused by having to err on the side of caution in designing economic aid that was sufficiently forceful. But inflation did not decrease, quite the contrary, it ended up being transferred to the price expectations of all economic agents. At that point, the Fed recognized that it had a problem and completed a remarkable U-turn in monetary policy. The market listened carefully and long-term interest rates (which had been contained within a range) began to rise sharply.

The war in Ukraine, renewed lockdowns in China and a Fed that, keeping in mind how difficult it was to raise interest rates during the last cycle, did not want to tighten prematurely, have ended in market tumult. It seems as if the „secular stagnation“ regime of the last decade; characterized by low demand, low growth and low inflation (as a result of an aging population, digitization and globalization) could be on the cusp of being replaced. Giving way to a new normal where demand would outstrip supply, employment would be plentiful and inflation would remain elevated.

The struggle between the two narratives can be seen in the 10-year US Treasury yield, hovering around the critical 3% level. That was the high-water mark of the previous decade. And given its role as a measure for long-term interest rate expectations, the fact that it was below 1% barely a year ago can be interpreted as a sea change in investors‘ view of the future macroeconomic environment.

Regime changes sometimes do happen, and the pandemic may have been the trigger to move from one state of the economy to another. But the fact that there is no fundamental reason for this transition should serve as a warning not to change investment thesis lightly. The current high inflation is an uncomfortable reality that we cannot ignore, but we should not think that it will become a permanent fixture of our lives.

Investors, unlike mindfulness practitioners and Amazon Prime customers, should try to resist the „Power of Now“. Investing is about delaying gratification and discounting the future. And the present matters only to the extent that it can be informative of the future. Focusing too much on the present, whether it is painful like now or rosy, can lead to poor investment decisions, and make us fall prey to panics and manias.

By the same token, investors have to be careful in not fast-forwarding the future too much. Reality unfolds at its own pace and turns out to be much more complex and surprising that what our minds can imagine beforehand. The no so „transitory“ nature of the bout of inflation is a very good reminder of how notoriously difficult is to forecast the future.

This delicate balance between present and future is complicated by the fact that information flows bit by bit. Macroeconomic data is released monthly at best, companies report their results quarterly, and the Fed meets every other month. But money never sleeps, and information gaps are filled by noise. Psychological dependence is akin to binge-watching: viewers devour each new episode eager to find out how it all ends, only to discover that they will have to wait for the next season.

At the moment, the thrill is whether inflation will finally subside, preventing the Fed from having to tighten too aggressively, or whether, on the contrary, will have to raise rates to a point that the economy breaks. At the moment, the data tells a story about stubborn inflation and a robust economy, which economic logic tells us cannot last for long.

But it will take time to find out how it all plays out. Inflation has gained a lot of momentum and is not going to slow down quickly. As for the impact of rising interest rates on growth, monetary policy works mainly through two transmission channels. A direct (and slower) one, increasing financing costs for consumers and corporations. And an indirect (faster) one, deflating the value of financial assets and real estate, inflicting a negative wealth effect on consumers.

For more than a decade the Fed has resorted to the second channel to support asset prices, always ready to reassure markets whenever there has been market turmoil. Today, however, the central bank remains conspicuously silent, waiting for markets to do much of the heavy lifting needed to rein in inflation.

Until the macroeconomic uncertainty begins to dissipate, markets continue to gyrate between two scenarios that, a priori, are opposite. If the main reason for the correction in equity markets until now had been the increase in interest rates, a recessionary environment should reverse (at least in part) said increase. This should help cushion the subsequent drop in corporate earnings as the economy slows down. This argument is most apparent for growth stocks, which have corrected much more due to rate hikes, and are less exposed to the business cycle.

However, what we are witnessing is that both narratives are feeding back each other. When macro data is released showing that inflation is not abating, markets fall as interest rates rise. And when on the contrary the data points to the economy slowing down, stocks also fall due to the potential impact on corporate profits.

This is not entirely irrational, since in the event that there is a recession, it is impossible to predict whether it will be deep or shallow. Just as we cannot put a date on when the supply-side shortages stoking inflation will disappear. But in the absence of data revealing enough to tip the balance in favor of one of the two scenarios, there is a growing disconnect between the impact that macroeconomic variables are having on company valuations, and the potential of the latter to generate benefits in the long term.

It is certainly very painful to see portfolios dragged down by the uncertainty of the present, but financial history shows us how, time and again, Corporate America always manage to grow through economic cycles. Investors need to be patient and look beyond the current market turmoil, knowing that in the long run the opportunity cost outweighs the downside risks. Or if we consider ourselves as mere viewers of a complex reality, we should not worry too much about how exactly the plot will unfold, since the end of this type of show is usually very similar.

* This document is for information purposes only and does not constitute, and may not be construed as, a recommendation, offer or solicitation to buy or sell any securities and/or assets mentioned herein. Nor may the information contained herein be considered as definitive, because it is subject to unforeseeable changes and amendments.

Past performance does not guarantee future performance, and none of the information is intended to suggest that any of the returns set forth herein will be obtained in the future.

The fact that BCM can provide information regarding the status, development, evaluation, etc. in relation to markets or specific assets cannot be construed as a commitment or guarantee of performance; and BCM does not assume any liability for the performance of these assets or markets.

Data on investment stocks, their yields and other characteristics are based on or derived from information from reliable sources, which are generally available to the general public, and do not represent a commitment, warranty or liability of BCM.