BY FERNANDO DE FRUTOS, CFA, PhD | 30 AUGUST 2022

- Powell’s long-awaited speech at the Jackson Hole symposium followed the expected script. In the intricate dance between central banks and financial markets, no news is, in a sense, news

- Equity markets responded to the Fed’s renewed inflation-fighting resolve with a big sell-off. Such a reaction seems more like a tantrum than a move justified by a change in economic fundamentals (given that long-term interest rates barely moved)

- Taming inflation expectations is essential to anchor long-term interest rates and thereby underpin both stock and bond valuations. But this entails inflicting short-term economic pain, the duration and intensity of which is difficult to quantify at this time

Financial markets are now part of popular folklore. Crowds gather in Omaha to worship their oracle, sports arenas are named after Crypto exchanges, and central bankers have become celebrities.

Last week, the once secluded meeting of central bankers in Jackson Hole had the media coverage of a major sporting event. This used to be a rather academic symposium, giving bankers the opportunity to socialize in a relaxed setting – somewhat akin to a cardiologists‘ conference. Last Friday, the anticipation for Chairman Powell’s speech was unprecedented.

As expected, he delivered a very scripted speech. As equally expected, was his reassurance that the Fed will not rest until inflation is under control, even if this means a slowdown in economic activity and a rise in unemployment.

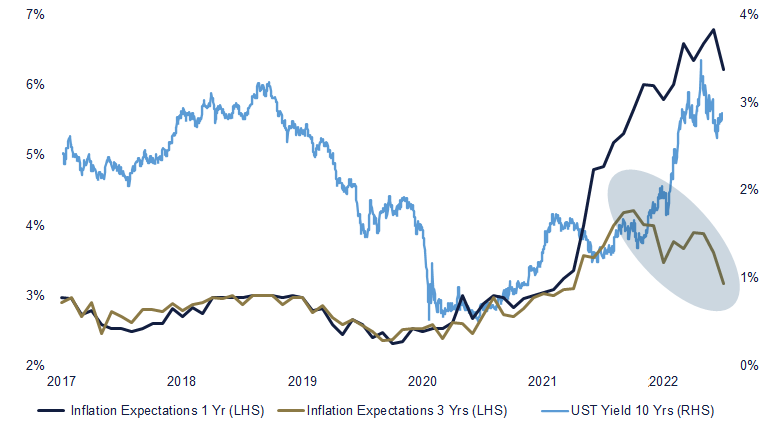

Any other message would have been a mistake, as the Fed has had to go all out just to start seeing inflation expectations fall (see chart at the bottom). In this sense, the selloff experienced on Friday is difficult to understand, unless it is seen as a mere tantrum for not getting any new piece of information.

A common problem with our institutions is that they have barely evolved from the days when they were run by the elites, with little or no accountability to the people. In the past, central banks were used to operating as they pleased; shrouded in an aura of secrecy, since most mere mortals did not understand the workings of monetary policy.

In today’s information age, they are now out in the open, where anyone can see that they are not infallible. Having lost much of their „auctoritas“, they now face increasing pressure to explain their movements to a constituency that has not elected them.

In recent decades, monetary policy has tried to improve transparency (although it seems hard to believe, until the mid-1990s, the Fed’s decisions were still not communicated to the public). Under Ben Bernanke, the Fed went one step further by setting an inflation target (something his predecessor Alan Greenspan always resisted). To provide visibility (and avoid disappointing markets) Janet Yellen resorted to „Forward Guidance“, to telegraph future movements.

However, with inflation out of control, transparency coupled with hard inflation targets means breaking news of economic pain. Chairman Powell tried to sugarcoat it by talking about „below-trend growth“ and „softening of labor market conditions“ but there is a clear risk that if mass layoffs occur as a result of the Fed’s policies, its independence could be jeopardized.

It is worth remembering that what is bad for the economy is not necessarily harmful for financial markets. In this sense, Powell’s speech should be seen as good news for investors. Judging from their response though, some of them were hoping for a „Fed Pivot“ to provide some short-term relief. The biggest risk investors face right now is not a recession, but that inflation expectations move to a structurally higher level (and thereby cause a regime change in interest rates).

In this regard, markets’ reaction last Friday can be divided into two camps. Bond markets kept their cool, with the 10-year US Treasury yield barely moving, in a nod to Powell’s resolve to fight inflation. Equity markets, meanwhile, acted more myopically, falling sharply in disappointment with a more “hawkish” Fed.

The Fed must remain on course, unaffected by political and media chatter; firmly tying its monetary policy to the future path of inflation. This implies that, as supply bottle-necks ease, the chances of a “soft landing” now depend on how fast (and how much) both labor and housing costs fall. This is something that the Fed can directly influence through rate hikes.

* This document is for information purposes only and does not constitute, and may not be construed as, a recommendation, offer or solicitation to buy or sell any securities and/or assets mentioned herein. Nor may the information contained herein be considered as definitive, because it is subject to unforeseeable changes and amendments.

Past performance does not guarantee future performance, and none of the information is intended to suggest that any of the returns set forth herein will be obtained in the future.

The fact that BCM can provide information regarding the status, development, evaluation, etc. in relation to markets or specific assets cannot be construed as a commitment or guarantee of performance; and BCM does not assume any liability for the performance of these assets or markets.

Data on investment stocks, their yields and other characteristics are based on or derived from information from reliable sources, which are generally available to the general public, and do not represent a commitment, warranty or liability of BCM.