The period of historically low interest rates we are currently experiencing is forcing investors to test unchartered waters, as valuations become greatly distorted when operating close to the zero interest rate bound. Theoretically, any financial asset can be valued as the expected value of all future cash-flows discounted at a rate which is the sum of the risk-free rate and a certain risk premia. When the risk free rate decreases towards zero, as has happened during the recent years as a result of the ultra-loose monetary policy implemented by central banks, the impact it has on valuations is increasingly large. In the extreme case, if markets would price no risk premia, valuations would tend to infinite in the current interest rate environment.

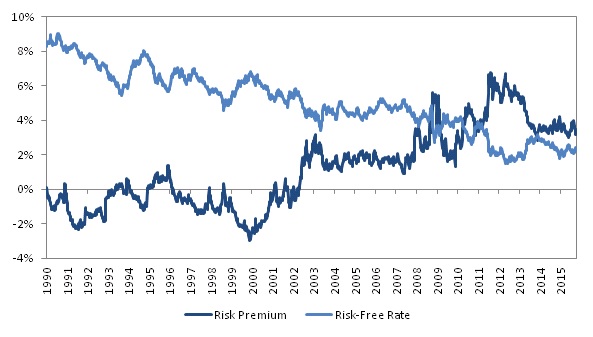

However, despite unconventional monetary policies have undoubtedly contributed to inflate asset prices, markets have remained relatively disciplined and, in fact, have responded to the decrease in the risk-free rate with an increase in the risk premia. This can be seen in the following graph showing both the evolution of the risk-free rate (proxied by the 10-year US Treasury rate) and the risk premia (measured as the difference between the earnings yield in the S&P 500 and the risk-free rate).

This compensatory effect probably implies that market participants have perceived low rates to be only of a temporary nature. Nonetheless, it can be observed that the inverse relationship between interest rates and risk premia lasted only until 2012 and since then the risk premia started to shrink as stock prices have kept rising faster than earnings. As a result, valuations are currently more exposed to changes in the risk premia, which is influenced by market sentiment, and hence the repeat of further episodes of market volatility like those experienced in August cannot be ruled out.

This document is for information purposes only and does not constitute, and may not be construed as, a recommendation, offer or solicitation to buy or sell any securities and/or assets mentioned herein. Nor may the information contained herein be considered as definitive, because it is subject to unforeseeable changes and amendments.

Past performance does not guarantee future performance, and none of the information is intended to suggest that any of the returns set forth herein will be obtained in the future.

The fact that MWM can provide information regarding the status, development, evaluation, etc. in relation to markets or specific assets cannot be construed as a commitment or guarantee of performance; and MWM does not assume any liability for the performance of these assets or markets.

Data on investment stocks, their yields and other characteristics are based on or derived from information from reliable sources, which are generally available to the general public, and do not represent a commitment, warranty or liability of MWM.

* This document is for information purposes only and does not constitute, and may not be construed as, a recommendation, offer or solicitation to buy or sell any securities and/or assets mentioned herein. Nor may the information contained herein be considered as definitive, because it is subject to unforeseeable changes and amendments.

Past performance does not guarantee future performance, and none of the information is intended to suggest that any of the returns set forth herein will be obtained in the future.

The fact that BCM can provide information regarding the status, development, evaluation, etc. in relation to markets or specific assets cannot be construed as a commitment or guarantee of performance; and BCM does not assume any liability for the performance of these assets or markets.

Data on investment stocks, their yields and other characteristics are based on or derived from information from reliable sources, which are generally available to the general public, and do not represent a commitment, warranty or liability of BCM.