• Omicron is just another variant of concern; but with a catchy name. There will be a Pi, a Rho and a Sigma, but it is very unlikely that any of them will cause an impact similar to that of Alpha; when it all began last year

• Optimism about our ability to deal with new variants and defeat the pandemic cannot be directly extrapolated to financial markets. Although equity indices recovered swiftly from the impact of the Delta variant during the summer, inflation dynamics are complicating the Fed’s job this time

• If governments overreact to the threat that the new variant poses to healthcare infrastructure, while economic agents prepare to further logistic disruptions, there is a risk that this economic cycle will be a short one. With such a level of uncertainty, we recommend avoiding tactical moves and remain invested in quality assets

Until last Friday, Omicron was only part of the vocabulary of crosswords aficionados and Greek scholars. However, despite the initial uproar caused by the announcement, the emergence of this variant was the closest to a sure thing to happen. Its inevitability was a consequence of the WHO’s decision to name variants of interest after the letters of the Greek alphabet, and the high likelihood of the virus turning endemic due to its very high transmissibility.

It is also a fact that the longer it takes to reach a level of immunity in the population that is sufficient to significantly slow down the spread of the virus, the more time it will have to mutate and find new ways of spreading. Sadly, despite having had the immense luck of developing highly effective vaccines in record time thanks to human ingenuity, an equally very human lack of solidarity is prolonging the problem: vaccine skeptics in rich countries, and insufficient doses available to developing ones.

No matter how well-intentioned the WHO was in changing its naming system for new variants (supposedly to facilitate public communication), there is little doubt that Omicron’s announcement was saluted by those with a direct interest in the pandemic lingering longer: the media and the pharma industry. A catchy, complex, and threatening name to sell more newspaper headlines and subscriptions, and a new opportunity to expand the vaccine business.

Equity markets tumbled on the news, and governments around the world rushed to show their preparedness to implement measures to contain the spread of the new variant; although we all know that it is still too early to know if Omicron represents a greater threat than Delta, or if the vaccines will lose their effectiveness.

Despite the absence of clinical studies and regardless of the number of mutations found in the new variant, it is highly unlikely that the world will return to the dark days of the spring of 2020. Back then we argued that our collective learning curve is much steeper than that of the virus, and since then that gap has only increased.

Time could have proved us wrong when it comes to investments in the short and medium term; especially if central banks and governments had not reacted so forcefully. However, when it comes to our ability to fight the virus, the prediction was a safe bet. Almost two years after it all started, we have a wealth of experience in preventing and treating the disease, as well as in rapidly scaling up healthcare infrastructure. And what is equally important, vaccines and infections have trained our bodies on how to fight the virus.

However, all this positivity about the course of the pandemic cannot be directly extrapolated to financial markets. Especially since a large part of this optimism is already reflected in the current valuations of stocks and corporate bonds. Therefore, any downside risk to the widely held scenario of a “V-shaped” economic recovery has the potential to weigh on them.

To this, we must add that there is a clear danger that the new variant will exacerbate the shock to the global supply chain caused by the virus. An unforeseen scenario by many companies that, in a never-ending effort to reduce costs, failed to properly calibrate both the risks associated with using suppliers from all around the world, and the perils of running “just-in-time” inventory management systems.

Supply and demand imbalances are responsible for the high inflation we are experiencing (or at least they are its initial cause), and threaten to trigger a tightening of monetary policy. A situation similar to that experienced with the Delta variant over the summer, but this time with the Fed’s finger much closer to the trigger.

Whether this will be yet another “buy the dip” opportunity or a trend reversal will depend on all economic actors keeping a cool head. This means that before resorting to new restrictions, governments are guided by clinical data and healthcare capacity, rather than headlines. Also, and perhaps more important at this time, that both consumers and producers do not respond up-fronting purchases in anticipation of further shortages, thereby exacerbating inflationary pressures.

Unfortunately for investors, human minds are far less predictable than a virus. The risk is that inflation and large fiscal deficits will also become “endemic” once a majority of the population concludes that the government must – and has the ability to – finance the economy indefinitely. However, if central banks retain their independence, they will try to prevent this from happening. Judging by the Fed’s reaction to the Omicron announcement, we could be starting to glimpse the beginning of a tough battle ahead between fiscal and monetary policy; something implicit in the Fed’s pivot back in July.

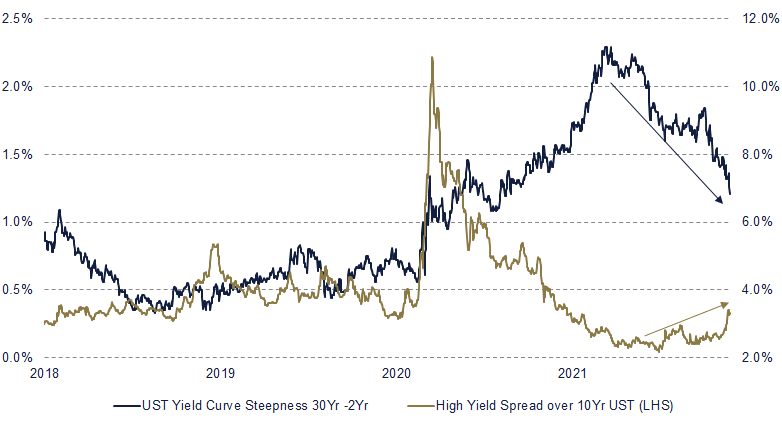

The longer current imbalances persist, the greater the risk that this business cycle will be much volatile and shorter than the previous two. Something that is starting to be reflected in traditional recession indicators, which are rising for the first time since the reopening (see graph below). With this in mind, we continue to believe that this is not the time for tactical bets on portfolios, but rather to stick to proven strategies: diversifying macroeconomic risks, sacrificing some potential appreciation for portfolio protection, and concentrating on quality assets.

BY FERNANDO DE FRUTOS, CFA, PhD | 1 DECEMBER 2021

* This document is for information purposes only and does not constitute, and may not be construed as, a recommendation, offer or solicitation to buy or sell any securities and/or assets mentioned herein. Nor may the information contained herein be considered as definitive, because it is subject to unforeseeable changes and amendments.

Past performance does not guarantee future performance, and none of the information is intended to suggest that any of the returns set forth herein will be obtained in the future.

The fact that BCM can provide information regarding the status, development, evaluation, etc. in relation to markets or specific assets cannot be construed as a commitment or guarantee of performance; and BCM does not assume any liability for the performance of these assets or markets.

Data on investment stocks, their yields and other characteristics are based on or derived from information from reliable sources, which are generally available to the general public, and do not represent a commitment, warranty or liability of BCM.