That pesky Bitcoin

- For reasons that are not yet clear, Bitcoin has managed to escape regulation for much longer than initially expected. But given its current market value, the risks from a transparency, investor protection and financial stability standpoint are simply too great to continue avoiding the regulatory radar.

- From a technological point of view, Bitcoin’s technology is becoming obsolete. The increasing cost of processing transactions makes it difficult to scale, and it is unlikely that it will ever replace traditional payment systems. And as a store of value, Bitcoin is constantly at risk of being replaced by a superior digital currency. One that can process transactions faster and more efficiently, and whose cryptographic base is more secure.

- Bitcoin is in part the result of an unprecedented marketing campaign; one that involves psychological warfare. But unfounded fears about a money debasement aside, the crypto craze is a symptom of the need for a digital overhaul of the financial system. We believe that the real opportunity is not in cryptocurrencies, but in investing in leading companies in the FinTech space.

One of the things I least like about having to die one day is that I will leave this world without being able to even conceive of the coming scientific, technological and social advances. Like a Cro-Magnon, ignorant of the Internet, quantum physics and the welfare state. To this, I must now add, that I would really hate to miss the end of the Bitcoin psychodrama.

For financial orthodoxy, cryptocurrencies are a kind of biblical plague that keeps returning with increasing periodicity. Back in 2016 we published a note about digital currencies, where we advanced a simple rule to value Bitcoin in the event that it were to replace gold one day. Under this assumption, the value of the cryptocurrency could range from $170,000 to $460,000. Unfortunately, I did not buy Bitcoins back then. And the reason that led me not to do so was that to achieve the same status as gold, the cryptocurrency would have to manage to escape two formidable enemies: regulatory control and technological obsolescence.

The elephant in the regulators room

Finance and nuclear power are probably the two most regulated industries in the world. That is why it is very difficult for practitioners to understand the “laissez-faire” of regulators towards cryptocurrencies. Central banks may fear that an attempt to regulate them may be seen as an admission of guilt for their own misdeeds; or simply that it is a matter of intellectual disdain for monetary ” aficionados”, who would eventually learn their lesson.

This is in stark contrast to the virulent backlash towards Libra, the digital currency (now called Diem) sponsored by a Facebook-led consortium. As soon as the cryptocurrency – impeccably designed from a monetary point of view – was announced, it came under strong criticism from both legislators and regulators. Prima facie, due to the risks it would pose from a money laundering and data protection point of view; but ultimately because of its potential to dethrone the US dollar.

Over the past two decades, the regulatory pendulum has swung toward more, not less, transparency. The US goes to great lengths to ensure that the settlement of all US dollar transactions takes place within its borders; in order to combat money laundering, terrorism, and compliance with sanctions.

In the fight for greater transparency, the US is not alone. The Financial Action Task Force is supported by the OECD and the G20. The introduction of FATCA and CRS has significantly cornered black money, forcing banks to disclose the beneficial owners behind bank accounts. Additionally, for only a few years, it is necessary to indicate the name of the beneficiary of a transfer, and not just the account number. Considering all this, Bitcoin seems like an aberration.

The looming regulation will not necessarily imply the demise of Bitcoin, but it will greatly reduce its use case as a currency outside of the traditional payments system. In fact, this is already happening and not because of regulation, but because of the risk inherent in buying and storing cryptocurrencies. Most investors who have acquired Bitcoins lately, have used traditional financial channels instead of anonymous crypto-wallets.

The other big regulatory trend has been toward greater investor protection. During the last decade, while investment in cryptocurrencies grew without controls of any kind, a wave of new regulations came into force (Investor Protection Law, MiFID, PRIIPs, etc.) aimed at controlling financial products offered to retail investors. While Bitcoin was just a curiosity outside the system, the protection seemed unnecessary. But the more investors it attracts and the more publicity is made about it, the more imperative it is for watchdogs to intervene.

Finally, there is the aspect of market integrity. Currency markets are closely policed to prevent manipulation. It is no coincidence that, in dealing rooms, FX traders are always the ones with the worst reputations (now we know that those who dealt with Libor were no saints either). Regulators have imposed hefty fines on banks, and jailed a number of individuals, for manipulating the currency markets. If this has been possible in the largest market by trading volume, it is easy to imagine what must be going on with Bitcoin.

All three regulatory alerts have been ignored while Bitcoin was nothing more than a funny topic of conversation that enlivened dinners in the upper echelons of finance. But with the cryptocurrency having passed the $50,000 mark, the risks are simply too great to be ignored. Bitcoin today is the Nirvana of rogue states, money launderers, and tax fraudsters, and it poses a real risk to financial stability. To give some perspective, the current market value of Bitcoin is approximately $1Tn. This compares with $7Tn in circulation (the so-called M1 monetary aggregate), $12Tn in deposits, and $21Tn in US Treasuries (roughly the size of the US economy). It’s easy to imagine that Janet Yellen and Jerome Powell are not cracking jokes about Bitcoin these days.

Technology ages faster than fashion

If alchemy was nothing more than bad science stuffed with philosophy, Bitcoin is bad economics combined with a promising, yet nascent, technology. Now gold can be created in the laboratory using nuclear reactions, although it is still far from being economically viable. The same can be said about the cryptocurrency, except that it cannot be used in jewelry.

If one thing characterizes technology in general, it is that there is nothing permanent about it. Today the Walkman is the coolest thing, but then comes the Discman, the iPod, Spotify… Innovation never ends; it is a constant race to do more, better and cheaper.

One of the most fascinating things about Bitcoin is its technological immobility. In its more than a decade of existence, Bitcoin has hardly undergone any modifications. Several cryptocurrencies have forked from Bitcoin to improve their performance, (with questionable success), but the founding principles of the blockchain remain largely unchanged.

In fact, judging from its applications so far, and despite all the initial excitement, you might think that the blockchain technology is hitting a dead end. However, it is still too early to reach this conclusion. Technological development is not linear. Sometimes a new technology stalls until another advance allows it to unleash its full potential (e.g., 4G until the introduction of the smartphone). At other times, the technology needs to go through a long journey of incremental improvements until it reaches a point where it becomes economical (e.g., solar power).

In economic terms, a technology can become successful if it is superior to the competition in at least one of two aspects: efficiency and / or scalability; epitomized by Moor’s Law and Metcalfe’s Law. Either functionality is improved and / or costs are reduced (e.g.: microchips, cars, etc.), or it has practically zero marginal costs and network effects are harnessed (e.g.: Google, Facebook, Aribnb, etc.)

In the case of Bitcoin, the two laws collide with each other. By limiting its amount to 21 million by design, the reward in Bitcoins for processing transactions progressively decreases, as the complexity of the blockchain increases. This enforced inefficiency causes Bitcoin miners to incur an ever-increasing cost in terms of energy consumption; and that the desired network effects can only be achieved if the price of Bitcoin continues to rise faster than the marginal cost of mining it. The limits to its scalability are now clear: with only a tiny fraction of the population transacting in Bitcoins, it is estimated that the associated energy consumption is equivalent to that of a country like Norway.

And what will happen in the year 2140, when all the Bitcoins have been mined (approximately 2.5 million remain to be mined). What will be the incentive to process a monster blockchain? Here, the most widely accepted hypothesis is that a transaction fee will have to be introduced to incentivize miners, and that it will be cheap because at that time there will be many of them. All this fanfare to end up with a traditional commission-based model, which will only be technically feasible if electricity (and microchips) are practically free by then?

Proponents argue that by then the network will be so large that it will have value on its own. But there is a fundamental aspect of network effects that challenges this idea. Successful network operators generally achieve scale by offering their services for free; in exchange for being able to collect user data, and / or place advertising. But the ultimate premise of Bitcoin is to protect the privacy of its users, thereby preventing the monetization of the network

And the problems do not end here. When you have a successful network, you have to defend it from the competition. You just have to see how Facebook has maintained its advantage by acquiring potential competitors like Instagram or WhatsApp. Digital currencies are undoubtedly the future of payments, but it is too early to know who will end up being the dominant players (states, decentralized cryptos, private companies) and what technology will ultimately prevail.

In short, anyone who owns Bitcoins as a store of value is constantly at risk of losing everything due to the emergence of a superior cryptocurrency. One that can process transactions faster and more efficiently, and whose cryptographic base is more secure. The latter aspect is not trivial, since quantum computing is already a reality. This means that most traditional cryptographic algorithms, such as the one used by Bitcoin, will someday no longer be secure. And while quantum computers may still be in their infancy, betting your savings against human invention is rarely a good idea.

The most successful marketing campaign ever seen

One of the things that should put us most on our guard about Bitcoin is the changing narrative behind it. Like a hair growth lotion that is also advertised as good for the immune system in case it doesn’t work. The sales pitch has evolved from something that will one day revolutionize the monetary system, passing through a store of value that protects against inflation, a new “asset class” alternative to gold that will sooner or later end up in all investment portfolios to, finally, a currency that large corporations will have no choice but to hold on their balance sheets – in the latter, Tesla has not been the pioneer, since organized crime has been long in the lead.

In fact, that a tech luminary like Elon Musk is buying Bitcoins is probably the strongest argument in favor of the cryptocurrency. But basing the merits of an idea on a person’s “auctoritas” takes us back to medieval philosophy. Aristotle was undoubtedly a genius, but as we know now, he was wrong about many things. We also know that Elon Musk is a master of free marketing, and that with this move he is probably trying to maintain Tesla’s lofty valuation, by association.

If someone approached you on the street, and tried to convince you to sell your house for a handful of cryptocurrencies (today the average house in the US costs around 6 Bitcoins), you would despise him as a fool or a con man. Common sense dictates that no one is buying cryptocurrencies out of necessity, as most people have access to stable coins with low inflation. The only reason to buy Bitcoin is simply the expectation that its price will continue to rise as more and more people want to buy it. And that is the purest possible definition of a bubble.

However, no matter how coolheaded you are, be aware that the constant bombardment of news about the meteoric rise of Bitcoin is causing you considerable psychological stress. A mechanism known as cognitive dissonance, which tempts us to modify our convictions. As the saying goes: “If you can’t beat them. Join them”. Institutional investors who are jumping on the bandwagon now are not doing so because they have discovered something new about Bitcoin, but because they fear being ridiculed for missing out; although they do not invest much for fear of the opposite…

For investors, probably the most effective medicine against these mind games is to narrow down where the real investment opportunity lies. This means forgetting about the great ambition of replacing fiat money or finding digital gold, and focusing on the great need for a digital revamp of the financial system.

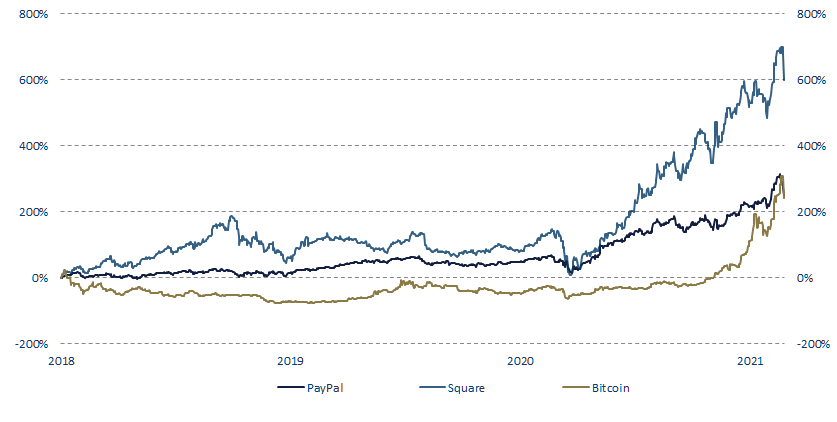

This revolution is being carried out by a bunch of innovative companies that vie to offer faster, cheaper and more convenient ways to carry out financial transactions. These are real companies, with real business models, operating cash flows, and proprietary products and technology. And as can be seen in the chart below, until recently, they were an equally profitable investment alternative to cryptocurrencies; with much less risk.

Fernando de Frutos – Chief Investment Officer

* This document is for information purposes only and does not constitute, and may not be construed as, a recommendation, offer or solicitation to buy or sell any securities and/or assets mentioned herein. Nor may the information contained herein be considered as definitive, because it is subject to unforeseeable changes and amendments.

Past performance does not guarantee future performance, and none of the information is intended to suggest that any of the returns set forth herein will be obtained in the future.

The fact that BCM can provide information regarding the status, development, evaluation, etc. in relation to markets or specific assets cannot be construed as a commitment or guarantee of performance; and BCM does not assume any liability for the performance of these assets or markets.

Data on investment stocks, their yields and other characteristics are based on or derived from information from reliable sources, which are generally available to the general public, and do not represent a commitment, warranty or liability of BCM.