BY FERNANDO DE FRUTOS, CFA, PhD | 17 JANUARY 2023

- The last three years have been completely abnormal. Today’s inflation is a byproduct of the pandemic, just as high interest rates are. The disappointing returns last year, like the exceptional two years prior, must also be seen in the same context. Sooner or later there will be a return to macroeconomic stability. The problem is that the price to pay for it can be a recession.

- A year after the Fed´s remarkable monetary policy U-turn, we are beginning to see the first effects on the economy. However, it is still too early to bet on whether it will be a hard or a soft landing. For now, consumers seem relatively insulated from the worsening economic environment, but it remains to be seen how they react when unemployment starts to rise.

- From an asset allocation standpoint, bonds shine in attractiveness. Stocks, by contrast, have gotten much cheaper from where they started a year ago. However, there is still uncertainty about how much corporate profits will fall. For this reason, bonds have an important role to play in portfolios, providing investors with a base of returns that helps cushion the volatility that will surely come from the equity part.

The one-year milestone for dividing time is deeply rooted in human nature, but it is generally too short to judge investments. However, at the beginning of the new year it is inevitable that we look back, and that we look to the future in said measure of time. Even more so after having experienced one of the worst years for investors in living memory.

Last year around this time, we had a blurry picture of what could happen. Both the economy and corporate earnings had enjoyed a record year of growth after the economy reopened. The price to pay for the strong demand was a sharp rise in inflation which, contrary to expectations, had proven not to be just a temporary phenomenon. Meanwhile, the Fed, still more concerned with economic growth than inflation, was preparing (very cautiously) to end its zero-interest rate policy.

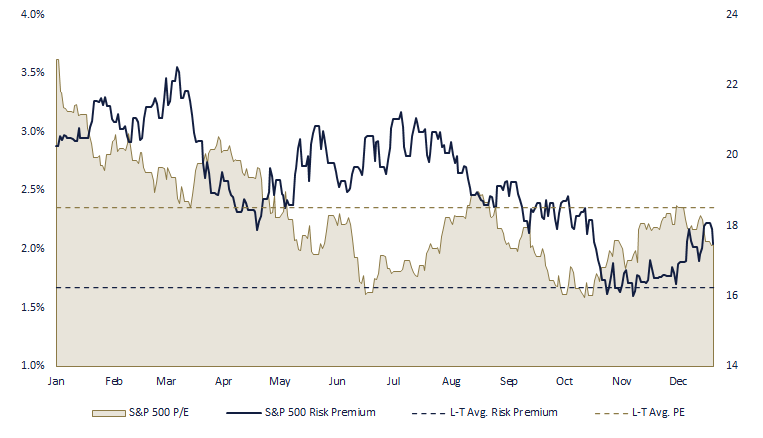

Against this backdrop, stocks looked expensive based on absolute valuation metrics (price to earnings), but attractive when considering their valuation relative to bonds (equity risk premium). On the other hand, bonds seemed vulnerable to interest rate hikes in the short end of the curve. While in the long-end, interest rates had normalized, and it seemed unlikely that they would continue to rise.

This was all before the war broke out in Ukraine, giving a fatal boost to inflation through energy markets. The consequences are well known to all. Inflation reached levels not seen in four decades and lasted long enough to end up spilling over the service sector. The Fed was then forced to raise interest rates at an unprecedented rate, causing equity and bond markets to correct in tandem. Something never experienced in such magnitude, and that caused large losses in portfolios, regardless of the mix between stocks and bonds.

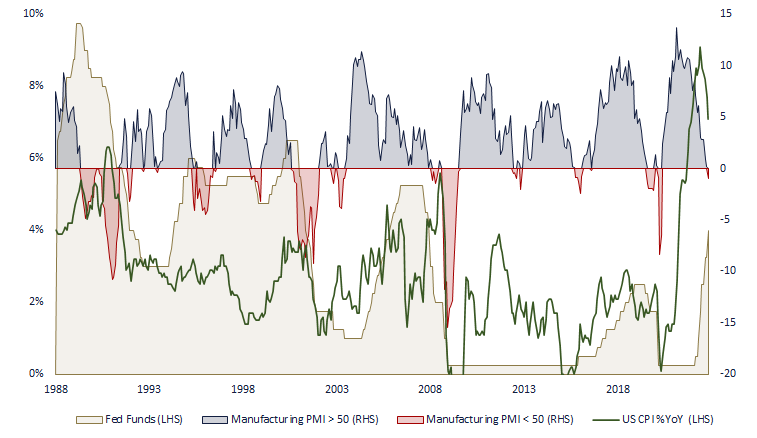

Typically, the Fed raises interest rates in measured steps to gauge their further impact on the economy. This was also the way to proceed in previous episodes of high inflation. Although back then, price pressures built up over time, like a tide, while this time, inflation manifested itself as a tsunami. As a result, policymakers, found themselves behind the curve and rushed to hike. The price they had to pay for such a steep tightening was to say goodbye to any chance to fine-tune their response.

It is easy to criticize the Fed now. It is true that they were slow to respond to the initial surge of inflation when the economy reopened. But considering that they were facing a completely new situation, erring on the side of caution seemed the most sensible course of action. Back then, the risk of the economy stalling was the main concern, while inflation was being caused mainly by supply-side constraints that seemed transitory in nature.

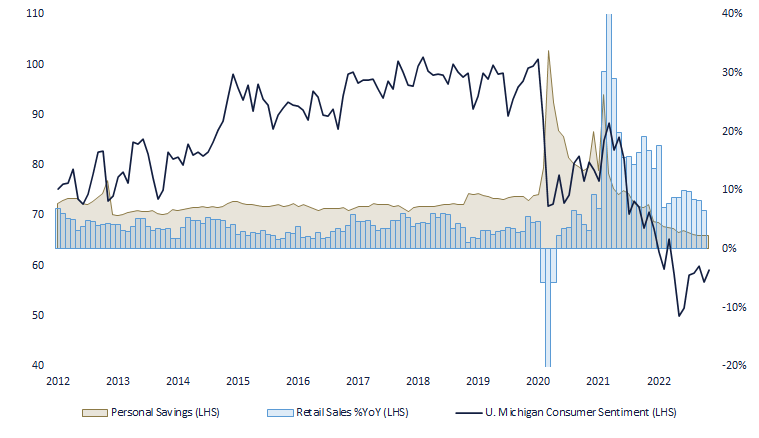

We now know that this prudent approach underestimated the boost to demand provided by an overly generous fiscal policy (also trying not to fall short of stimulus). But transfers alone cannot explain why consumption remains strong amid a worsening macroeconomic situation. Certainly, the savings accumulated during the pandemic have helped to maintain the level of spending despite the loss of real disposable income. But the pandemic also seems to have altered, at least temporarily, the propensity to save among consumers.

All this explains the resilience of the services sector (although leading indicators warn us of a potential slowdown) as opposed to the manufacturing sector, which began to contract a few months ago. The fact that inflation has started to decline since the summer, while the economy has so far emerged relatively unscathed from the sharp increase in interest rates, has provided support to equity markets.

It is highly unlikely that inflation will return to the Fed’s 2% target without the economy slowing down. To win the battle against inflation, the labor market must loosen up. It remains to be seen if when unemployment starts to rise consumers will keep their cool. That will make the difference between a “soft landing” and a “hard landing”.

The level of uncertainty is much higher than usual since this time there will be no quick fix. Over the past few decades, whenever the economy went through a soft patch, central banks were quick to come to the rescue. This time, however, inflation is so exorbitantly high that the Fed will only reverse course (before completing its mission) if it perceives risks to financial stability.

Looking into the new year ahead, with interest rates close to peaking and credit spreads well above their historical average, a bad year for high-quality bonds is hardly conceivable. As for equities, large corrections are often followed by strong rallies, the main exception being the years after the dot-com bubble. On this occasion it is quite questionable that there was a bubble in the stock market in the first place, and if there was one (from a P/E point of view), the brutal adjustment experienced during the year should have deflated it.

The starting situation in 2023 is almost a mirror of last year. Stock prices fell sharply while corporate profits continued to rise. This has meant that valuations have fallen drastically in absolute terms. On the other hand, interest rates have risen sharply, reducing the relative attractiveness of stocks versus bonds. This means that bonds are again called upon to play a pivotal role in portfolios, providing a base that helps cushion equity volatility.

With investors so heavily focused on how inflation evolves, as well as the sort of “landing” the economy ultimately experiences, volatility is all but guaranteed. It is impossible to know if the market has already bottomed out. But considering the magnitude of the correction experienced, and that the stock market tends to go up in the long run, there is no other option than to fasten our seatbelts until the turbulence ends.

* This document is for information purposes only and does not constitute, and may not be construed as, a recommendation, offer or solicitation to buy or sell any securities and/or assets mentioned herein. Nor may the information contained herein be considered as definitive, because it is subject to unforeseeable changes and amendments.

Past performance does not guarantee future performance, and none of the information is intended to suggest that any of the returns set forth herein will be obtained in the future.

The fact that BCM can provide information regarding the status, development, evaluation, etc. in relation to markets or specific assets cannot be construed as a commitment or guarantee of performance; and BCM does not assume any liability for the performance of these assets or markets.

Data on investment stocks, their yields and other characteristics are based on or derived from information from reliable sources, which are generally available to the general public, and do not represent a commitment, warranty or liability of BCM.