BY FERNANDO DE FRUTOS, CFA, PhD | 6 SEPTEMBER 2022

• As inflation continues to show no signs of abating, the pressure on the Fed to act decisively is mounting. The true purpose of the “jumbo” interest rates hikes is to send an unequivocal signal to all economic agents, and keep inflation expectations anchored. Even at the cost of engineering a recession.

• The recent volatility in US the Treasury market cannot be explained by fundamentals alone. Yields in the long end of the curve should have fallen in response to increased recession risk, but the opposite has happened. A possible explanation may lie in the recent disorderly movements in currency markets.

• The old saying “Don’t fight the Fed” is a warning to those who ignore the direction of its monetary policy. Right now, this can apply both to investors who are betting that the Fed won’t be able to control inflation, and to other central banks who are moving in the opposite direction.

Financial markets do not obey logic. These are complex systems, subject to the investment decisions of many individual participants. From large institutional investors to meme-stocks mobs. Each party receives and assimilates information differently and decides whether to act on it.

Price movements are solely determined by the marginal buyers and sellers present at any given time. The trigger to trade can be a change in fundamentals (economic data, corporate news, geopolitical events, etc.) or in liquidity conditions (from central banks pumping or withdrawing money, to personal monetary affairs).

Fundamentals resemble the tides, ultimately determining long-term returns. Liquidity flows, by contrast, act like waves and ripples. But the latter should not be ignored. Financial markets are inherently chaotic systems. Powerful storms can form unexpectedly from the flapping wings of the proverbial butterfly; last time embodied in the form of subprime mortgages.

Liquidity flows are difficult to observe and interpret, with a few exceptions. Central bank liquidity injections (“Quantitative Easing”) are intended to be predictable. Another important recurring flow is the hoarding of US Treasuries by countries that generate large current account surpluses, such as China, Japan, and Middle Eastern nations.

Recently, however, we are observing a reversal of these flows. The Fed, in its mission to kill inflation, is quietly winding down its balance sheet, thereby reducing demand for Treasuries. Coincidentally, the confiscation of Russian reserves due to the war in Ukraine has caused non-aligned countries to rethink their appetite for US Treasuries.

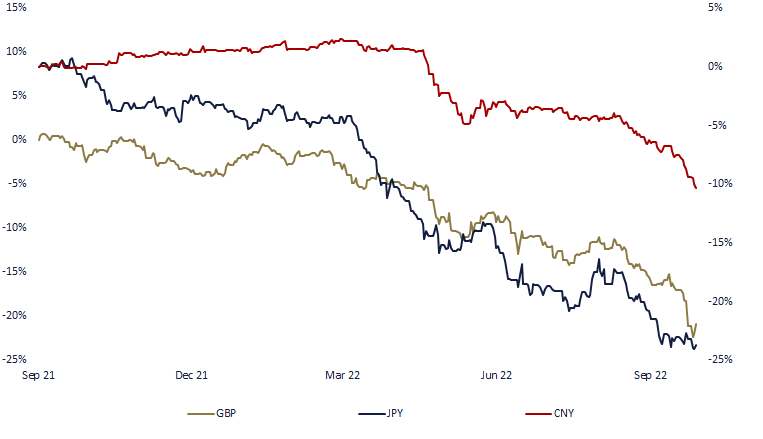

To further complicate matters, the Bank of China´s (BoC) monetary policy is diametrically opposed to the Fed´s. Hindered by an ineffective response to the pandemic coupled with a real estate crisis, the

BoC is lowering interest rates to stimulate its economy. The Bank of Japan (BoJ) also diverges by maintaining its “yield curve control” strategy unchanged.

As the interest rate gap between these countries and the US widens, their currencies are taking a beat. This has forced the BoJ to intervene in the foreign exchange market to prop up the yen. And it has also caused the BoC to relax the trading band of the Renminbi.

In both cases, this implies selling their dollar reserves, which are invested in US Treasury bonds. This duo has been joined by the Bank of England (BoE), which last week had to intervene hastily to calm the tumult created around the pound after an ill-fated tax reform.

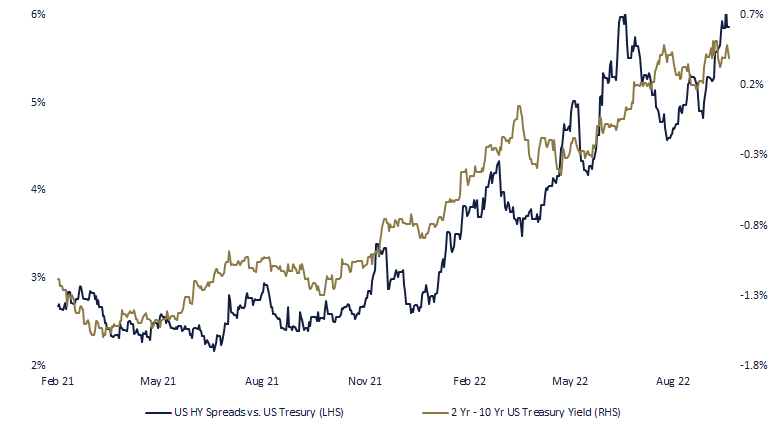

Unsurprisingly, we have seen unusual selling pressure in US Treasuries recently, causing the long end of the yield curve to decouple from fundamentals. The latter dictate that if the Fed does whatever it takes to reduce inflation, the economy is going to take a sure hit. With the economy in recession, sooner or later inflation will subside, and the Fed will have to lower interest rates.

This explains why the yield curve has dramatically inverted, and credit spreads have widened. In the absence of relevant macroeconomic data, only flows can explain the recent rise in long-term interest rates. A mere anomaly, if it weren’t for the fact that the 10-year Treasury yield is the single most determining variable in the financial system. That is why, when it approached the 4% level last week, stocks plunged to new lows.

Watching major central banks in disarray is cause for concern. Interventions to defend your own currency are often doomed to fail, since it forces the country to burn through its (limited) reserves. The old market adage “Don’t fight the Fed” can also be applied to central banks. Sooner or later, the BoC and BoJ will be forced to let their currencies depreciate, or align their monetary policy with the Fed.

In the meantime, investors should also not double guess the Fed’s determination to crack down on inflation. Equity valuations have compressed massively by a combination of high interest rates and expectations of falling corporate earnings as the economy stalls. The unknown is how deep the soft patch will be, and how long it will last. But if the Fed is successful, and the economy resumes its growth path, current valuations will prove to be a very attractive entry point for long-term investors.

* This document is for information purposes only and does not constitute, and may not be construed as, a recommendation, offer or solicitation to buy or sell any securities and/or assets mentioned herein. Nor may the information contained herein be considered as definitive, because it is subject to unforeseeable changes and amendments.

Past performance does not guarantee future performance, and none of the information is intended to suggest that any of the returns set forth herein will be obtained in the future.

The fact that BCM can provide information regarding the status, development, evaluation, etc. in relation to markets or specific assets cannot be construed as a commitment or guarantee of performance; and BCM does not assume any liability for the performance of these assets or markets.

Data on investment stocks, their yields and other characteristics are based on or derived from information from reliable sources, which are generally available to the general public, and do not represent a commitment, warranty or liability of BCM.